ASEAN countries have committed to long-term net-zero targets but recent trends show that they are tackling decarbonization largely in an independent manner which is costly and inefficient.

South East Asia has a wide range of renewable energy resources including solar, wind, hydropower and geothermal. Cross-border interconnection has a crucial role to play during the clean energy transition to achieve decarbonization as it will enable sharing of low-cost renewable resources across different locations in the region.

DNV recently released a white paper (ASEAN Interconnector Study: taking a regional approach to decarbonization) where it examined the potential benefits and implications of ASEAN cross-border interconnectors during the energy transition towards a fully decarbonized power sector in South East Asia in 2050. Quantitative modelling was developed with the aim of minimizing the overall net present cost of such a transition. The model determines the location and type of renewable generation across the region on a least-cost basis, based on localized production costs and on the available energy transport routes and transport costs between nodes.

Assumptions/Models

Modelling has been done based on the expected demand in 2050, while respecting existing power development plans where available to provide a baseline of domestic generation and renewables potential. The model used for this study seeks to optimize decarbonization from a system perspective and allows for the use of hydrogen production to capture surplus renewable production and a regional hydrogen network with centralized storage to redistribute this across the region and achieve 100% decarbonization of power generation. This study demonstrated the benefits of a cooperative or fully regional approach to decarbonization while emphasising cost reductions and reduced renewable energy requirements.

In addition, the study considers two main technological routes as possible decarbonization pathways depending on advancements achieved over the years: 1) repurposing dispatchable fossil-fuel power plants with low-carbon fuels (e.g. hydrogen) and 2) electricity storage (i.e. battery energy storage systems (BESS) and pumped storage hydropower).

To evaluate the potential benefits of a more interconnected South East Asia, DNV modelled 3 scenarios for each ASEAN country aiming to achieve 100% decarbonization by 2050:

- Individual approach: Countries independently strive to decarbonize using their own resources.

- Moderate interconnection: Based on the ‘ASEAN RE Target Case,’ this scenario includes cross-border power interconnectors with limited transmission capacity and no hydrogen network.

- Regional cooperation: Unconstrained resource-sharing between countries, involving power interconnectors and hydrogen networks.

Findings

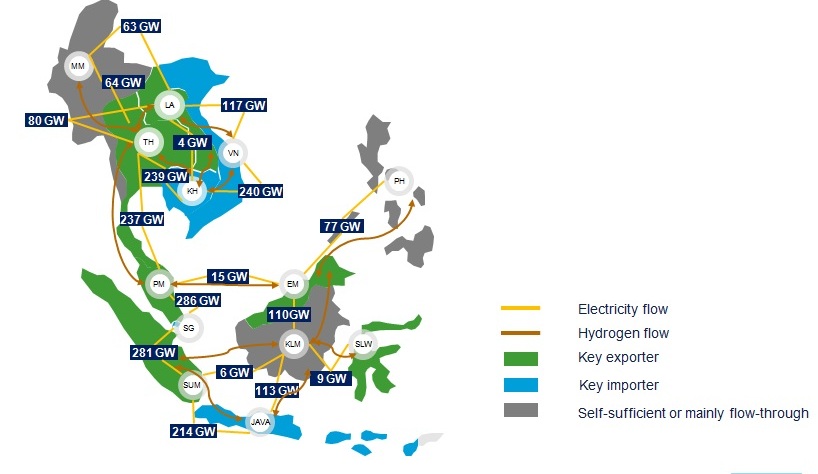

The model results show that regional cooperation with cross-border interconnectors brings economic benefits to the region by reducing overall resource requirements and spatial footprints. Additionally, full resource-sharing via cross-border interconnectors will cause significant shifts in the ASEAN energy landscape. The large interconnector capacities allow for significant quantities of energy to be transported from countries with high renewable potential to countries with less diverse supply or lower-quality resources, paving the way for several to become main exporters or importers. Countries with diversified supply resources of solar, wind, and hydropower, such as Thailand and Lao PDR, will be the engines of the transition as large-scale exporters of clean energy. Power and hydrogen will start to flow, from north to south and west to east, to countries with less diverse supply or lower-quality resources.

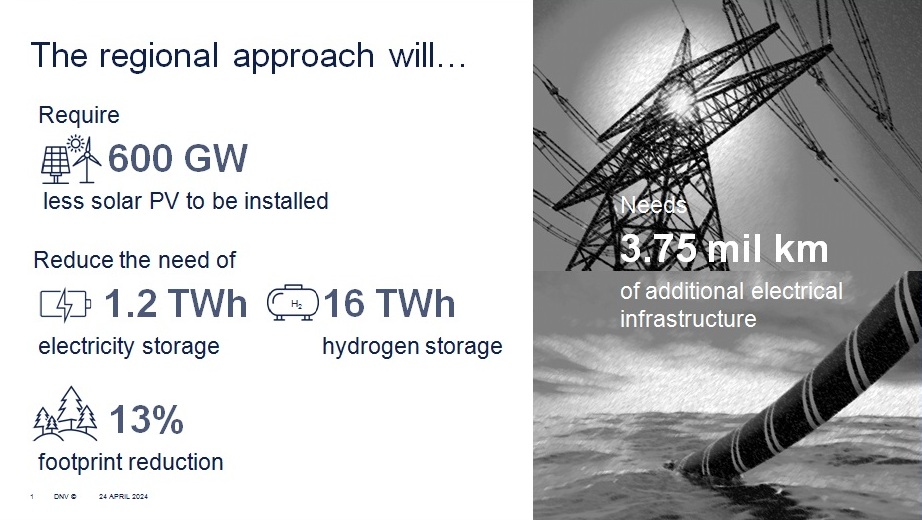

The energy transition with full Regional Cooperation can reduce the required total installed solar generating capacity by up to 600 GW (20%) by 2050 compared to the Individual Approach where each country does not consider regional interconnection. In addition, the region would need 1.2 TWh less electrical storage and 16 TWh less hydrogen storage. One of the largest benefits is that the need for hydrogen storage could be reduced by 24% and 58% under Moderate Interconnection and Regional Cooperation, respectively, when compared with the Individual Approach. Regional Cooperation also reduces by 13% the spatial footprint required for South East Asia’s energy transition, largely due to the reduction in solar capacity needed for a fully interconnected ASEAN.

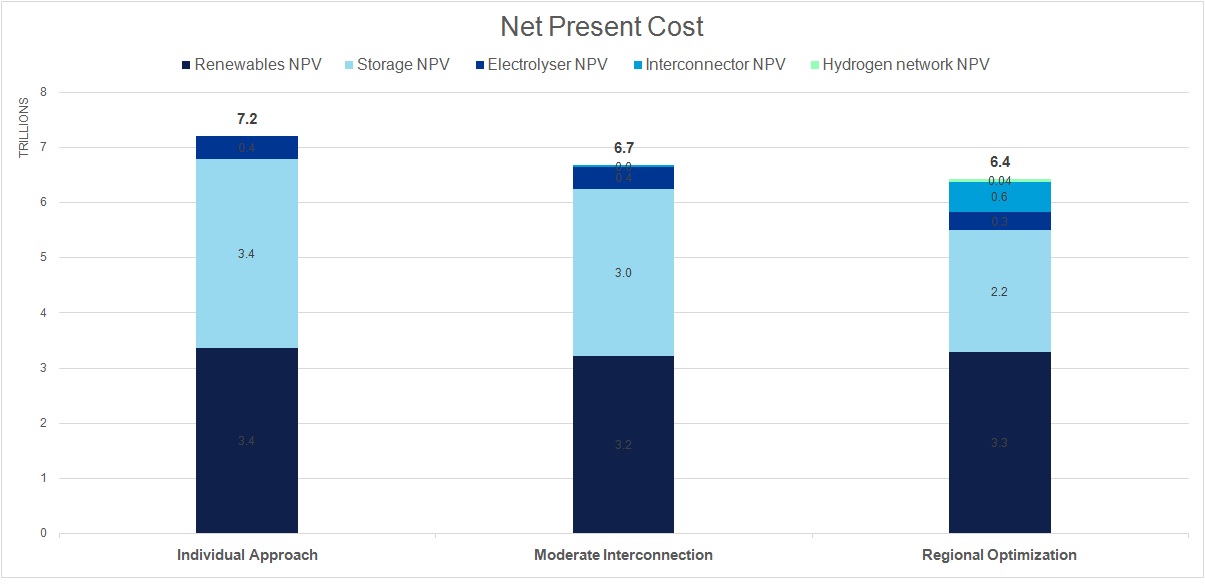

Regional Cooperation brings the lowest overall cost among the three scenarios. Approximately USD 0.8 trillion (approximately 11%) can be cut from the overall net present cost of ASEAN decarbonization by 2050 compared to the approach in which each country pursues decarbonization individually without relying on interconnectors. In absolute terms, the relative net present cost (NPC) for decarbonizing a fully interconnected ASEAN region models at USD 6.4 trillion against USD 7.2 trillion for the Individual Approach scenario.

The main trade-off for the economic benefits is that such a transition would require significant amounts of additional electricity interconnection capacity involving up to 3.57 million kilometres of cable. This is roughly an additional 29% of global demand for transmission cables compared to what was projected in DNV’s Energy Transition Outlook.

Challenges and potential barriers in developing ASEAN interconnectors

Despite the significant economic benefits of cross-border interconnection and its role in decarbonizing power supply, there are potential challenges and barriers to fully developing ASEAN interconnectors. With the view from key stakeholders in the ASEAN power sector, the challenges are related to policy and regulatory, financial and economic, and technical perspectives that involve governmental and private stakeholders in the power sector.

From the governance, policy and regulatory framework perspective, power grids are natural monopolies; so, developing cross-border interconnectors requires political support and the necessary regulatory frameworks. A lack of policy (or government) support and regulatory frameworks are the main barriers for developing power grids, rather than technical and economic. Despite ASEAN’s ambitions for regional interconnectivity, there is still a gap in the regulatory framework and coordination among relevant jurisdictions. These challenges are associated with:

- A diverse set of policies and market structure among ASEAN countries

- Uncertainty in political will and institutional arrangements

- Lengthy regulatory process in permitting and licensing

From a financial and economic perspective, developing interconnectors entails significant capital investment and financial risk due to the relatively long lead time. Main concerns include, among others, uncertainties on funding source, ownership structure, and remuneration mechanisms. The power industry is still vertically integrated in most ASEAN member states, meaning that the investment in power grids needs support from relevant governmental and private stakeholders. In addition, many electric utilities which own and operate the grid may have limited financial resources to invest in grids, including cross-border interconnectors.

In terms of technical challenges, there are concerns over energy security due to unreliable domestic grids in some countries, particularly with renewables growing rapidly. Hence, many countries choose to upgrade domestic grid capability prior to cross-border infrastructure. There is also limited technical expertise in building and operating cross-border interconnections as it will involve long-distance power transfer with highly specialized transmission equipment. Technical limitations exist regarding the amount of renewables that can be integrated into the grid since the extent to which the flexibility resources (i.e. BESS, hydropower plants) contribute to system stability via system inertia and reserves varies depending on the type of technology. Consequently, countries may prefer to retain a larger share of generation within their domestic networks to increase domestic network stability. This will also largely depend on the type of technology used to connect between countries – either high-voltage alternating current (HVAC) or direct current (HVDC) transmission. The use of HVAC transmission lines will increase the size of the balancing area, allowing for increased system stability, but comes at the cost of less economically efficient power transfer over larger distances compared to HVDC. A mix of both technologies will likely be the most suitable approach, but this will have to be investigated in more detail to provide an optimal balance of security and cost.

Action plan and priorities to support the development of cross-border interconnection in ASEAN

There are three main action areas to address the main challenges and accelerate the development of ASEAN interconnectors. In each action area, there are main priorities and plans to overcome the challenges. The three main action areas are:

- Coordinate and harmonize the regional policy framework – To overcome the barriers in developing cross-border interconnectors, the policy and institutional framework as well as regulatory process will require several changes at the national and regional level with the aim to increase coordination and harmonization between countries. There is also a need for a platform to support regional coordination. The priorities for increasing coordination and harmonizing the policy framework include:

- establishing a taskforce with clear responsibilities (short term);

- conducting small scale pilots (short to medium term) and

- setting a consistent and harmonized ASEAN power trading framework (medium to longer term).

Gaining knowledge and experience from other regions and sectors is also a priority in the short to medium term.

- Clarify and address financial risks and uncertainties- Investment in cross-border interconnectors in South East Asia is one of the major challenges due to the amount of grid infrastructure required and the uncertainties over financial resources. The priorities for accelerating financing and investment in cross-border interconnectors include:

- policy support for interconnector financing and de-risking investment (short term);

- providing remuneration certainty and clarity on transmission ownership (short to medium term) and

- regulatory streamlining for technology to provide clear regulatory guidance (short to longer term).

- Secure supply chain and resource development- Developing a cross-border interconnector requires a secure and diversified supply chain to deliver the components at the speed required to meet the targets. The significant requirement of grid infrastructure, cables, and renewables capacity to achieve a fully decarbonized regional power market by 2050 can place significant stress on the future supply chain. Inadequate supply-chain capacity raises concerns about a lack of local manufacturing capabilities in many regions. Priorities for ASEAN member states to strengthen the local supply chain include:

- establishing a local manufacturing supply chain of grid components (short to longer term)

- setting common procurement processes and technical specifications (short to medium term) and

- developing local human resources in the short to longer term.

In summary, DNV’s ASEAN Interconnector study aims to push the envelope towards full decarbonization, highlighting the benefits and addressing the challenges related to the implementation of an interconnected ASEAN grid.

Authors: This article is jointly authored by Chea Wae Sean Ooi, Consultant, Energy Markets & Strategy, Energy Systems APAC, DNV; Dr. Peerapat Vithayarichareon, Principal Consultant, Energy Markets & Strategy, Energy Systems APAC, DNV; and, Mats de Ronde, Team Lead, Energy Markets & Strategy, Energy Systems APAC, DNV

Also read: DNV Launches Industry Project For HVDC Transmission In US

To download the full report, please click on the following link or scan the QR code:

DNV ASEAN Interconnector Study (Access to Full Report)