Hectic activity was seen in the interstate transmission system (ISTS) development space during the first half (H1: April to September) of FY25, with a record number of schemes awarded under the tariff-based competitive bidding (TBCB) route.

According to a special study by T&D India, a total of 14 ISTS schemes were formally awarded under the TBCB mechanism during H1FY25, which is from April 1, 2024 to September 30, 2024.

Formal award indicates the official transfer of project SPV from the bid process coordinator, which is either PFC Consulting Ltd (PFCCL) or REC Power Development & Consultancy Ltd (RECPDCL) to the successful bidder.

Apart from the 14 ISTS-TBCB projects formally awarded, there were four ISTS-TBCB schemes for which the letter of intent has been handed over to the winning bidder, but the formal transfer of project SPV was pending, as of September 30, 2024.

Going by the performance in H1 and the current bidding pipeline, FY25 (April to March) is likely to be the most hectic year so far for the ISTS-TBCB space. In FY24, a total of 23 ISTS-TBCB schemes were formally awarded in the whole of FY24 – a number that would be easily surpassed in FY25.

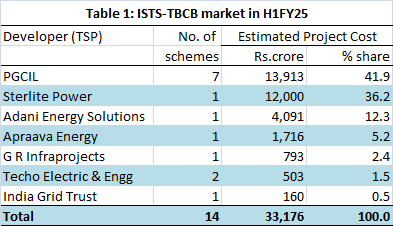

PGCIL gets most

The 14 ISTS-TBCB projects awarded in H1FY25 were distributed amongst seven developers. The distribution veered towards Power Grid Corporation of India Ltd (PGCIL) that won as many as seven of these 14 projects. The remaining seven were thinly distributed amongst six developers that included established players like Adani Energy Solutions Ltd and Sterlite Power. While relatively new entrants like India Grid Trust, Apraava Energy and G R Infraprojects Ltd recorded more success in H1 of FY25, the period also saw Techno Electric & Engineering Co Ltd re-entering the ISTS-TBCB space with two wins.

SPVs pending transfer

The four ISTS-TBCB schemes pending formal transfer, as of September 30, 2024, included three in which PGCIL has received the letter of intent. The fourth scheme “Paradeep Transmission Ltd” would be eventually transferred to Tata Power, marking the private power utility’s debut in the greenfield ISTS-TBCB space. In each of the four cases, PFC Consulting Ltd (PFCCL) is associated as the bid process coordinator.

In normal course, the formal transfer of SPV from the BPC to the successful bidder is expected to take place within ten days of issuance of the letter of intent (LoI). In the case, of Paradeep Transmission Ltd, Tata Power received the LoI on August 3, 2024 and it is quite intriguing to note that the project SPV was not transferred by PFCCL, even by September 30, 2024.

Market share by project cost

In the case of one scheme, Khavda Phase IV (7 GW), Part C, the project cost is understood to be revised during the bidding process to around Rs.12,000 crore from Rs.5,340 crore as originally estimated by NCT. This scheme was won by Sterlite Power — its sole ISTS-TBCB win in H1FY25. Thanks to the high project cost, Sterlite Power enjoyed a market share of around 36 per cent. (See Table 1)

Annual tariff

The aggregate tariff of the 14 ISTS-TBCB schemes awarded in H1FY25 was Rs.33,417.61 million. These tariffs of the 14 ISTS-TBCB schemes formally awarded in H1FY25 varied from Rs.152.50 million to as high as Rs.13,148.08 million.

Thus, when one sees the market share in terms of aggregate tariff of schemes awarded, Sterlite Power commanded a 39.3 per cent share despite having won just one scheme. PGCIL came second with 35.5 per cent though it had a much larger number of wins – at seven. (Please note that in official reports, transmission tariffs are conventionally denoted in “Rs.million” for better resolution.) [See Table 2]

In the context of the TBCB philosophy, it is the tariff quoted by the bidders on which the final selection depends. In practice, the tariff is the annual transmission charge that the developer (TSP) earns from the ISTS scheme during the project lifecycle – from the time of project commissioning (scheduled commercial operations date or SCOD) up to the end of the concession period, which is usually set at 25 years. The transmission charges are paid by the long-term transmission customers (LTTC) envisaged in the transmission service agreement (TSA). In normal course, the tariff quoted by the developer stays constant throughout the validity of the TSA.

The tariff of an ISTS scheme is directly proportional to the project cost, and effectively determines the return on investment (RoI) that the developer seeks to derive by building, owning and operating the ISTS scheme during the concession period.

Role of BPCs

Of the 14 ISTS-TBCB schemes formally awarded in H1FY25, as many as 11 had REDPDCL as the bid process coordinator (BPC), with PFCCL handling the remaining three. As indicated earlier, all the four schemes where the LoI has been issued but formal transfer of SPV was pending as of September 30, 2024, have PFCCL as the BPC.

Case of re-bidding

A striking feature of the ISTS-TBCB market in H1FY25 was the re-tendering of “Rajasthan Part I Power Transmission Ltd.” This project, estimated to cost around Rs.12,700 crore (as estimated by NCT) and involving deployment of HVDC technology-based infrastructure, was re-tendered in August 2024 after the original tendering process that was initiated in July 2023 was annulled by bid process coordinator RECPDCL. In fact, the original bidding process was in a very advanced stage with PGCIL emerging as L1, before the annulment.

Under the fresh bidding process, now underway, RECPDCL expects to finalize the bidder by October 28, 2024 and the formal transfer of project SPV is expected to take place on November 7, 2024.

Had the “Rajasthan Part I” project not come up for re-bidding, it would have been formally awarded by September 30, 2024. In which case, the dynamics of the ISTS-TBCB market in H1FY25, in terms of aggregate project cost, tariffs, market shares, etc, would have been radically different from what they are now.

Surpassing FY24 achievement

Going by the current bidding pipeline, it strongly appears that the ISTS-TBCB market will turn even more buoyant in H2 (October to March) of FY25. According to T&D India estimates, there are at least 30 ISTS-TBCB schemes under various stages of bidding and for most of them, the formal transfer of SPVs is expected to take place in H2FY25. Besides, the four ISTS-TBCB schemes pending transfer as of September 30, 2024 (discussed above), are most likely to be formalized in the coming weeks, contributing to the H2FY25 achievement.

In all likelihood, FY25 will by far surpass the achievement of FY24 in terms of number of ISTS-TBCB schemes formally awarded, aggregate project cost and transmission charges. In FY24, by T&D India estimates, a total of 23 ISTS-TBCB schemes were awarded out of which PGCIL had won ten. The total estimated project cost of the 23 schemes stood at around Rs.38,150 crore and the aggregate tariff was Rs.45,445.42 million. Going by aggregate tariff of ISTS-TBCB schemes, around 74 per cent of the FY24 level has already been attained in just the first half (H1) of FY25.

Newer application areas

It is important to note that forthcoming ISTS-TBCB schemes include quite a few with HVDC technology. They will therefore have high project cost and tariff. Secondly, H2FY25 will also see the emergence of ISTS schemes for newer application areas like feeding RE power for pumped storage projects (lifting of water) and for green hydrogen/ammonia producing plants. ISTS schemes dedicated to evacuation of hydropower and even nuclear power are also under bidding, and which are likely to be awarded in the remaining part of FY25.

At this juncture, it is worth observing that there is likely to be some pre-project activity in H2FY25 with respect to wind energy evacuation offshore Gujarat and Tamil Nadu. While offshore wind energy evacuation will be a new dimension on India’s power transmission landscape, the initial transmission schemes will be developed by PGCIL under the regulated tariff mechanism (RTM) mode. The TBCB modality could be considered only in future projects.

Also read: ISTS-TBCB Report Card for Q1FY25: Three awarded, none completed

Featured photograph (source: G R Infraprojects Ltd) is for representation only