Power Grid Corporation of India Ltd (PGCIL) is seen clearly dominating the ISTS-TBCB market, according to a special study by T&D India.

The study shows that PGCIL has a share of 60 per cent in the aggregate estimated project outlay of ISTS-TBCB schemes that are currently under construction.

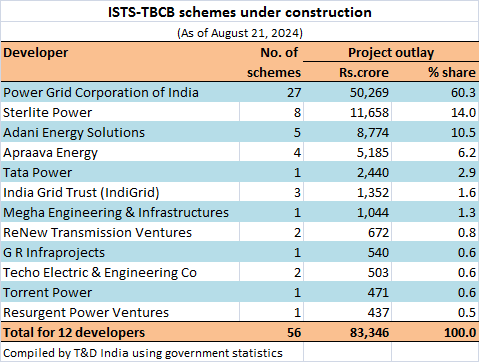

The study is based on 56 interstate transmission system (ISTS) schemes that have been awarded under the tariff-based competitive bidding (TBCB) route, and which are currently under construction. The aggregate project outlay of these 56 schemes is an estimated Rs.83,346 crore.

PGCIL currently has a portfolio of 27 schemes with an aggregate outlay of Rs.50,269 crore, which earns the company a share of 60 per cent in terms of project outlay. With respect to number of schemes, PGCIL’s share is nearly 50 per cent.

Sterlite Power ranked second with a share of 14 per cent in aggregate project outlay (see table), followed by Adani Transmission Ltd with 10.5 per cent.

Ranking fourth is Apraava Energy with a portfolio of four schemes with a total estimated project outlay of Rs.5,185 crore. Apraava Energy is a relatively new entrant in the greenfield power transmission development space having won its first set of projects in August 2023.

Tata Power, which made a rather delayed entry in the ISTS-TBCB market, currently has one scheme but with a fairly large outlay of Rs.2,440 crore. This has earned Tata Power the fifth rank. Tata Power is also partly associated with another ISTS-TBCB scheme being developed by Resurgent Power Ventures, in which Tata Power has minority equity holding.

Developer base

As of August 21, 2024, the developer base associated with the ISTS-TBCB market had 12 entities, which is by far the largest set of developers that the ISTS-TBCB market has seen so far.

Over the past 3-4 years, there has been a steady stream of new entrants like India Grid Trust (IndiGrid), Megha Engineering & Infrastructures, ReNew Transmission Ventures, G R Infraprojects, Techo Electric & Engineering Company, Torrent Power and Resurgent Power Ventures. These developers currently have just one or two projects under development, and that too medium-sized ones. However, their presence definitely contributes to enhancing the diversity of ISTS-TBCB developer base. It is also encouraging to note that some of developers like IndiGrid and G R Infraprojects have even fully commissioned their first ISTS-TBCB scheme.

Inclusion of schemes

An ISTS-TBCB scheme is considered to be under construction if the project SPV has been formally transferred to the successful developer, and which has not been fully commissioned. An ISTS-TBCB scheme is taken to be “under construction” even if one or more underlying elements of the overall scheme have been commissioned. For this study, schemes that were not fully commissioned up to July 31, 2024, have been considered.

The study has included schemes where the project SPV has been formally transferred till August 21, 2024. Specifically, the study does not include ISTS-TBCB schemes were a developer has been merely declared L1 or has been issued the letter of intent, by the bid process coordinator.

It may also be noted that out of the total 56 schemes under study, in two cases, the schemes were acquired by other developers, whilst still under construction. Adani Energy Solutions Ltd acquired one scheme from Megha Engineering & Infrastructures Ltd while Resurgent Power Ventures took over an ailing scheme originally won by Essel Infraprojects. All the remaining 54 schemes represent first-hand wins by the developer concerned.

Towards a higher market share

As clarified earlier, this study takes into account only those ISTS-TBCB schemes where the project SPV has been formally handed over to the successful developer. It is interesting to note that as of August 21, 2024, there were at least nine ISTS-TBCB schemes where a bidder has been declared L1 or has been issued the letter of intent. Significantly, of these nine schemes, PGCIL is associated with as many as six. The remaining three have been clinched one apiece by Adani Energy Solutions, Tata Power and G R Infraprojects.

It can be easily seen that when these schemes are formally transferred, the market share of PGCIL will rise even further from the current 60 per cent, more so because the aggregate outlay of these six schemes is significantly large, estimated at well over Rs.12,000 crore.

Editor’s Note: The project outlay of an ISTS-TBCB scheme is based on cost estimates provided by National Committee on Transmission (NCT) whilst approving the scheme, or as estimated by Central Electricity Authority (CEA) when the scheme comes under CEA’s monitoring purview.