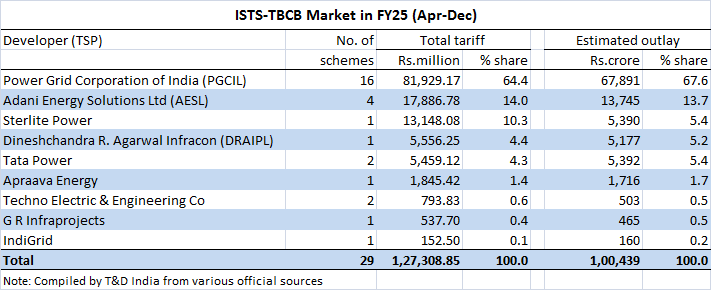

Power Grid Corporation of India Ltd (PGCIL) clearly dominated the ISTS-TBCB market accounting for a tariff share of over 60 per cent during the first nine months (April to December) of FY25.

According to a special study by T&D India, PGCIL won 16 out of the 29 interstate transmission system (ISTS) schemes awarded under the tariff-based competitive bidding (TBCB) route during the period April 1, 2024 to December 31, 2024.

PGCIL’s market share worked out to 64.4 per cent in terms of aggregate transmission tariff and 67.6 per cent in terms of estimated total project outlay. (See table).

The study covered ISTS-TBCB schemes where the selected developer formally acquired the project SPV from the respective bid process coordinator (BPC), which is either REC Power Development & Consultancy Ltd (RECPDCL) or PFC Consulting Ltd (PFCCL). Specifically, it does not include schemes in the pre-formal award stage where the BPC has named the L1 bidder or has issued the letter of intent (LoI) to the selected developer.

With PGCIL wresting 16 schemes, the remaining 13 schemes were sparsely distributed among as many as eight developers. It is also noteworthy that PGCIL was seen to be in the final race for each of the 29 schemes awarded.

PGCIL’s biggest win was “Khavda V-A Power Transmission Ltd” that was historical on several counts. It was the first TBCB project involving HVDC technology, and the biggest TBCB project in terms of project outlay (around Rs.25,000 crore) as well as transmission tariff (Rs.40,828.67 million per year).

In terms of tariff-based market share, Adani Energy Solutions Ltd (AESL) ranked second with 14 per cent. AESL clinched four ISTS-TBCB schemes during the period under review, with aggregate tariff of Rs.17,886.78 million and total project outlay of around Rs.18,000 crore.

Sterlite Power won just one scheme – Khavda IV C Power Transmission Ltd – but thanks to its high tariff of Rs.13,148.08 million, the company had a tariff-based share of 10.3 per cent.

Tata Power landed two schemes with aggregate transmission tariff of Rs.5,459.12 million and estimated project outlay of Rs.5,392 crore. This earned the private utility a market share of 4.3 per cent in terms of tariff, and 5.4 per cent with respect to project outlay.

New entrants

The first nine months of FY25 saw one new entrant – Dineshchandra R. Agarwal Infracon Pvt Ltd (DRAIPL) making its debut in the power transmission development space. Similarly, Techno Electric & Engineering Company Ltd re-entered the ISTS-TBCB market where it had debuted way back in 2011.

New infrastructure

The 29 ISTS-TBCB schemes under discussion, distributed among nine developers, envisage a total transmission line network of around 14,800 ckm and aggregate transformation capacity of over 1,20,000 MVA. PGCIL, through its 16 schemes, will be responsible for around 62 per cent of this new infrastructure creation – in terms of both lines and substations. The total capital expenditure of these 29 schemes is estimated to be over Rs.1 lakh crore (Rs.1 trillion) and the transmission service providers (developers) of these 29 schemes, once commissioned, stand to earn annual revenue (transmission charges) of around Rs.12,730 crore, collectively.

Role of BPCs

Of the two bid process coordinators, RECPDCL handled 18 ISTS-TBCB schemes as against 11 schemes by PFCCL, during the period under review. As indicated earlier, this study covers those ISTS-TBCB schemes that were formally handed over by the respective BPCs to the winning developers.

Imminent formal awards

According to estimates made by T&D India, there are at least five ISTS-TBCB schemes that are in the pre-formal award stage where either the winning developer has been named L1 or has been issued the letter of intent. These schemes are likely to be formally awarded during Q4 (January 1, 2025 to March 31, 2025) of FY25. Here, PGCIL is associated with three schemes with AESL and G R Infraprojects Ltd each having one scheme to their credit. In the case of AESL, the scheme in question is “Rajasthan Part I Power Transmission Ltd” that will be only the second HVDC-centric transmission scheme to be awarded under the TBCB mechanism. Thanks to this capital-intensive scheme, AESL is most likely to see its market share, in terms of tariff and project outlay, improve significantly by the end of FY25.

Busiest year

It can be easily seen that FY25 (April to March) will be the busiest year ever for ISTS-TBCB activity. The 29 schemes awarded in the first three quarters (April to December) have already surpassed the 23 schemes awarded in FY24. Further thanks to at least two large HVDC-based schemes already awarded in the period, FY25 will also end up with a record aggregate capital outlay associated with ISTS-TBCB schemes. Speaking of HVDC schemes, at least one such, housed under “KPS III HVDC Transmission Ltd” is likely to be formally awarded in Q4 of FY25.

ISTS-TBCB completions

Though data of commissioning of ISTS-TBCB schemes is not available for December 2024, available official statistics suggest that five such projects were commissioned in the first eight months (April 1, 2024 to November 30, 2024) of FY25. PGCIL and Sterlite Power had two projects each, with Renew Transmission Ventures contributing one. The total infrastructure created by these five ISTS-TBCB schemes is estimated to be 1,746 ckm of lines and 2,320 MVA of transformation capacity.

Editor’s Note: This study covers only interstate transmission system (ISTS) schemes awarded under the tariff-based competitive bidding (TBCB) route. It does not cover ISTS projects under the regulatory tariff mechanism (RTM) modality, or intrastate transmission system (InSTS) schemes whether TBCB or RTM.

It is reiterated that in the context of this special report, developers “winning” or “securing” projects implies that the developer has acquired the project SPV from the bid process coordinator (BPC). Emergence of L1 or issuance of letter of intent (LoI) by the BPC does not tantamount to “winning” a project, in the context of this report. All the primary data used in this report has been sourced from official and publicly available sources.