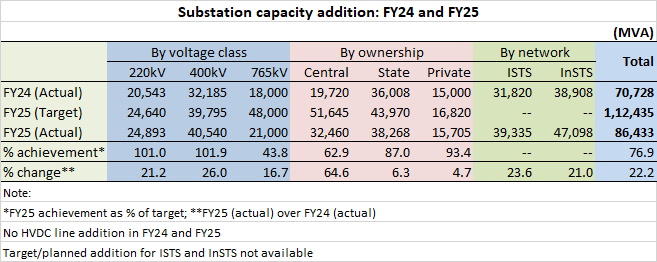

India added an impressive 86,433 MVA of transformation (substation) capacity in FY25 – a quantum that was 22.2 per cent more than the 70,728 MVA added in FY24.

The FY25 performance on the substation front was in pleasant contrast with the transmission line sector where the FY25 achievement represented the worst performance in several years. (Read T&D India’s story “FY25 sees lowest transmission line addition in recent history,” dated April 14, 2025)

The 86,433 MVA worth of substation capacity added in FY25 was nearly 77 per cent of the planned addition of 1,12,435 MVA. The shortfall came about mainly in the 765kV segment where the 21,000 MVA actually added in FY25 was less than half of the 48,000 MVA planned.

The overall performance was bolstered by the 220kV and 400kV voltage categories where actual addition in FY25 surpassed the targets. (See table).

Central government agencies (mainly Power Grid Corporation of India Ltd but also including relatively small contributions by Damodar Valley Corporation) did well to commission 32,460 MVA of substation capacity, which was an impressive 64.6 per cent higher than the achievement in FY24 (19,720 MVA). However, this ownership group could achieve only 62.9 per cent of the planned addition of 51,645 MVA. As explained earlier, this shortfall was largely due to some 765kV substations that failed to commission in FY25. (PGCIL deals with interstate/interregional grids where 765kV form the backbone.)

Of the 86,433 MVA of new substation capacity commissioned in FY25, around 45 per cent was on the interstate transmission system (ISTS) grid while a larger 55 per cent was towards intrastate (InSTS) grids.

The 39,335 MVA added on the ISTS side in FY25 marked a solid 23.6 per cent growth over FY24 when 31,820 MVA was commissioned. Similarly, substation capacity addition on the InSTS network was 21 per cent higher in FY25, year-on-year.

Interacting with T&D India, industry players explained while right-of-way constraints generally exist for power transmission-related infrastructure, they are more pronounced in the case of transmission lines where the geographical footprint is much larger, unlike in substations. Further, in substation capacity expansion projects, land provision is usually made at the time of building the original substation. This helps in swifter execution of such brownfield expansions.

PGCIL

Speaking of PGCIL alone, it added 31,515 MVA of new substation capacity in FY25, falling short of the 50,700 MVA planned. This unrealized difference of 19,185 MVA, it is learnt, is from projects that are in advanced stage of completion. These projects are likely to commission in the early part of the current fiscal year, FY26, and as such, would have a positive bearing on PGCIL’s overall performance in FY26.

Private sector

The private sector did well to commission 15,705 MVA of substation capacity in FY25, meeting 93.4 per cent of the planned addition, and recording a 4.7 per cent growth over the performance in FY24. Significant contributors included Adani Group, Resonia, IndiGrid and Megha Engineering. Independent RE generators also commissioned sizeable transformation capacity in FY25, mainly associated with ISTS connectivity of their RE generation projects.

Cumulative status

As of March 31, 2025, India’s overall transformation capacity of 220kV or higher stood at 13,37,513 MVA (or around 1,337 GVA), growing nearly 7 per cent from its comparable level in 2024.

[Note: This story takes into account substations of 220kV or higher, only. Featured photograph (source: MPPTCL) is for representation only.]