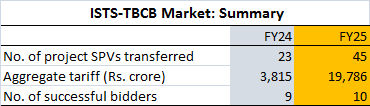

Fiscal year FY25 that closed on March 31, 2025 has been a record year for the ISTS-TBCB market, on several counts.

Based on an exclusive study by T&D India, FY25 saw as many as 45 interstate transmission system (ISTS) schemes being awarded under the tariff-based competitive bidding (TBCB) mechanism.

The study includes only those schemes where the project SPVs were formally transferred to winning developers by the respective bid process coordinators (BPC), during the period April 1, 2024 to March 31, 2025. Specifically, it does not look at ISTS-TBCB schemes where a developer has been named L1 or has been issued the letter of intent.

The aggregate tariff envisaged by these 45 schemes stood at a whopping Rs.19,786 crore. This was a quantum jump over FY24 when 23 schemes with aggregate tariff of Rs.3,815 crore were formally acquired by winning developers.

PGCIL: Most successful

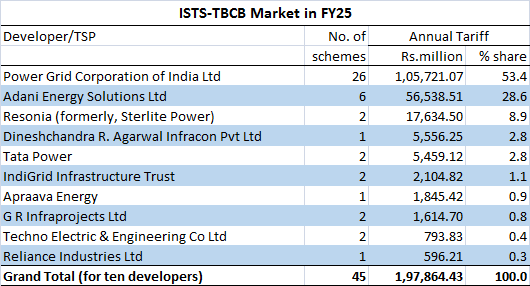

Power Grid Corporation of India Ltd (PGCIL) was the most successful developer winning as many as 26 schemes with a tariff-based market share of 53.4 per cent (see table). Adani Energy Solutions Ltd (AESL), with six ISTS-TBCB wins, ranked second – both with respect to number of schemes and aggregate tariff. AESL’s market share was 28.6 per cent with Resonia (formerly Sterlite Power) ranking third with a share of 8.9 per cent.

These three top players together enjoyed nearly 91 per cent tariff market share, leaving the remaining 9 per cent to be shared among seven developers, including two debutants – Dineshchandra R. Agarwal Infracon Pvt Ltd (DRAIPL) and Reliance Industries Ltd. Between them, these seven developers acquired 11 schemes.

Mega schemes

FY25 will also be remembered for having seen the award of India’s very first HVDC-based power transmission project awarded under the TBCB route. This distinction goes to PGCIL’s winning “Khavda V-A Power Transmission Ltd” with a record tariff of around Rs.4,083 crore. The magnitude of this tariff can be best appreciated by the fact that it exceeded the combined tariff of all the 23 ISTS-TBCB schemes awarded in FY24.

Another distinction was the award of India’s first HVDC project awarded to a private sector entity, under the TBCB framework. It was Adani Energy that earned this distinction when it won “Rajasthan Part I Power Transmission Ltd” at a tariff of Rs.3,557 crore.

RE dominates

Based on the aggregate tariff of the 45 ISTS-TBCB schemes awarded, the tariff corresponding to transmission schemes related to evacuation of renewable energy (including hydropower) represented around 90 per cent. The two mega HVDC schemes discussed above also pertained to RE evacuation. ISTS-TBCB schemes for RE evacuation were largely located in Rajasthan and Gujarat, apart from other RE-rich states like Maharashtra and Karnataka.

Bidder community

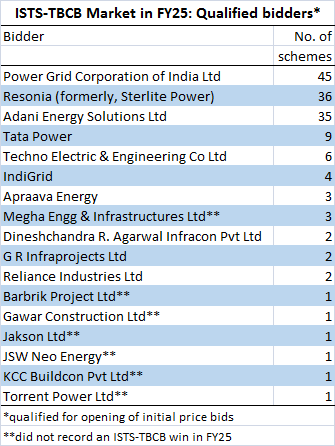

Interestingly, one scheme “Transmission scheme for integration of Bijapur REZ in Karnataka” housed under “Bijapur REZ Transmission Ltd” saw as many as nine bidders qualifying for opening of price bids, which included new names like Barbrik Project, Gawar Construction, KCC Buildcon and Jakson. None of these made their presence felt in any other ISTS-TBCB scheme awarded in FY25. The Bijapur REZ scheme was finally awarded to G R Infraprojects Ltd (GRIL). Interestingly, GRIL qualified for opening of price bids for two schemes, and won both of them.

As mentioned earlier, two entities – Reliance Industries Ltd and Dineshchandra R. Agarwal Infracon Pvt Ltd (DRAIPL) – made their debut in the ISTS-TBCB space in FY25. Similarly, Techno Engineering & Electric Co Ltd re-entered the ISTS-TBCB market. Kolkata-headquartered Techno had a portfolio of three ISTS-TBCB schemes, including two co-owned, which was eventually divested.

On the other hand, developers that won at least one scheme in FY24 but could not do so in FY25 included Torrent Power and Megha Engineering & Infrastructures Ltd.

Project outlay

Based on preliminary estimates, the 45 ISTS-TBCB schemes transferred in FY25, will entail aggregate capital investment of over Rs.1,54,000 crore. The project cost estimates are those made by National Committee on Transmission (NCT) at the time of structuring the project. There is bound to be revision in these cost estimates when the project comes up for implementation.

These 45 ISTS-TBCB schemes, once again based on preliminary estimates, will see the creation of around 20,150 ckm of transmission lines and around 2,13,500 MVA. This transmission infrastructure will largely be in the 765kV and 400kV class, and will also include ±800kV HVDC infrastructure, thanks to the two mega schemes discussed above.

The deluge of schemes awarded in FY25 has had a tremendous impact on the overall portfolio of ISTS-TBCB schemes, currently under construction. In FY25, according to T&D India estimates, seven ISTS-TBCB schemes were fully commissioned. With 45 ISTS-TBCB schemes awarded in FY25, the net addition in FY25 works out to 38 schemes. As of March 31, 2025, a total of 78 ISTS-TBCB schemes were under construction with nearly half of these awarded in FY25 alone.

RECPDCL has a larger share

In FY25, REC Power Development & Consultancy Ltd (RECPDCL) enjoyed a large pie of the ISTS-TBCB market handling 26 out of the 45 schemes transferred to winning developers. RECPDCL also had the distinction of handling both the mega HVDC schemes awarded in FY25. Thanks to this, RECPDCL had a majority share of nearly 75 per cent in terms of aggregate tariff of ISTS-TBCB schemes transferred in FY25.

In FY24, the only other bid process coordinator PFC Consulting Ltd (PFCCL) had played a bigger role than RECPDCL, both in terms of number of ISTS-TBCB schemes handled as well as the aggregate tariff associated with schemes awarded that year.

Only two entities– REC Power Development & Consultancy Ltd (RECPDCL) and PFC Consulting Ltd (PFCCL) – currently act as bid process coordinators for ISTS-TBCB schemes. BPCs have an important role in pre-project activities like preparing the survey report, and in conducting the bidding process. The role of a BPC ends when the project SPV of an ISTS-TBCB scheme, which is originally incorporated as a wholly-owned subsidiary of the BPC, is transferred to the winning developer.

It may be mentioned that RECPDCL is a wholly-owned subsidiary of REC Ltd, while PFCCL is similarly related to Power Finance Corporation Ltd (PFC). Further, REC Ltd is a subsidiary of PFC with the parent owning little over 52 per cent of REC’s equity capital.

Epilogue

With 45 ISTS-TBCB schemes and an aggregate tariff of nearly Rs.20,000 crore awarded, it is unlikely that FY25 will be rivalled in terms of number of schemes or tariff, for a long time to come.

Consider this. As of March 31, 2025, there were just around 20 ISTS-TBCB schemes under various stages of bidding. Besides, the number of ISTS-TBCB schemes being cleared by NCT, at least during recent meetings, has been dropping. There are currently no mega schemes in the planning stage, comparable to the two HVDC schemes awarded in FY25, except for one costing around Rs.12,000 crore and housed under “KPS III HVDC Transmission Ltd.”

Mega schemes like the Leh-Kaithal HVDC scheme or the offshore wind evacuation schemes in Gujarat and Tamil Nadu are being developed by PGCIL under the RTM route. Though these will imply significant augmentation of India’s power transmission infrastructure, they will have no bearing on the ISTS-TBCB market.

Another factor that could impinge upon prospects of the ISTS-TBCB market, albeit mildly, is the lack of response for certain TBCB schemes. In FY25, at least two ISTS-TBCB schemes saw just one bidder in the final stage. As per the existing norms, there should be at least two bidders for the selection process to be termed as “competitive bidding” in spirit. To obviate indefinite delay in infrastructure creation, CEA in FY25 devised a working rule where such stranded ISTS-TBCB schemes could be awarded under the regulated tariff mechanism (RTM) framework. This potentially means that a portion of ISTS schemes in future could fall out of the TBCB spectrum, of course without impinging on infrastructure development.

Intrastate schemes gaining ground

Speaking of the TBCB philosophy, there are incipient signs that this framework could see growing presence in the development of intrastate transmission system (InSTS) schemes. While state governments have generally not subscribed to the TBCB mode for intrastate grid developments, it is encouraging to see a state Maharashtra now pursuing TBCB, with at least seven InSTS schemes coming up for bidding. This adds to the list of states like Madhya Pradesh and Uttar Pradesh where the TBCB framework has contributed to significant infrastructure development of their intrastate grids.

It is also worth observing that RECPDCL and PFCCL, which have immense experience in the ISTS space, are now being appointed as bid process coordinators by state governments for InSTS schemes. This could streamline the bidder selection process and ensure expeditious award of projects. The emergence of the TBCB framework in intrastate grids also provides opportunity to power T&D contractors, especially the local ones that are familiar with state-level ground realities, to groom into transmission service providers.